About Manuel Amunategui

Data scientist with over 20-years experience in the tech industry, MAs in Predictive Analytics and

International Administration, co-author of Monetizing Machine Learning and VP of Data Science at SpringML.

From consulting in machine learning, healthcare modeling, 6 years on Wall Street in the financial industry, and 4 years at Microsoft, I feel like I’ve seen it all. And this has opened my eyes to the huge gap in educational material on applied data science. Like I say:

It just ain’t real 'til it reaches your customer’s plate

I am a startup advisor and available for speaking engagements with companies and schools on topics around building and motivating data science teams, and all things applied machine learning.

Reach me at amunategui@gmail.com

|

Exploring Some Pair-Trading Concepts with Python

Resources

Hi there, this is Manuel Amunategui- if you're enjoying the content, find more at ViralML.com

In this post, I want to share some simple ways of comparing stocks that are presumed related. My recommended approach for finding related companies is to use your own domain expertise. The second option is to use a site based on fundamental analysis that shows related companies (Google it, they’re lots out there like tipranks.com). I don’t recommend using pair-trading scanners as you’ll lose your shirt if you aren’t knowledgeable about the stock and sector - trader beware!

Once you have a few stocks in mind, you’re good to continue on with this exercise. Here we will use the ‘pair-trading’ classics of Coca-Cola vs. Pepsi, and FedEx vs. UPS.

Note: Everything discussed here is for educational purposes only.

import glob, os

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import matplotlib.dates as mdates

Load market data for FDX, UPS, KO, PEP

There are plenty of sources to get free stock market data, Yahoo Finance is one of them. But all those who will want to do some serious research in this area should not rely on free data. You will eventually need a safe, reliable and currated source of stock data - no shortcuts here.

To access current data, you can manually download the files from Yahoo Finance. For example, if you wanted to get the latest historical prices for Apple, simply enter the following link:

https://finance.yahoo.com/quote/FDX/history?p=FDX

And then find and click the "Download Data" link, it will default to one year of end-of-day market data. Run through this process for all four stocks listed in the title and save the four CSV files in a directory named 'data'.

# find the data directory and extract each CSV file

path = "data/"

allFiles = glob.glob(os.path.join(path, "*.csv"))

np_array_list = []

for file_ in allFiles:

df = pd.read_csv(file_,index_col=None, header=0)

# get symbol name from file

df['Symbol'] = (file_.split('/')[1]).split(".")[0]

# pull only needed fields

df = df[['Symbol','Date', 'Adj Close']]

np_array_list.append(df.as_matrix())

# stack all arrays and tranfer it into a data frame

comb_np_array = np.vstack(np_array_list)

# simplify column names

stock_data_raw = pd.DataFrame(comb_np_array, columns = ['Symbol','Date', 'Close'])

# fix datetime data

stock_data_raw['Date'] = pd.to_datetime(stock_data_raw['Date'], infer_datetime_format=True)

stock_data_raw['Date'] = stock_data_raw['Date'].dt.date

# check for NAs

stock_data_raw = stock_data_raw.dropna(axis=1, how='any')

# quick hack to get the column names (i.e. whatever stocks you loaded)

stock_data_tmp = stock_data_raw.copy()

# make symbol column header

stock_data_raw = stock_data_raw.pivot('Date','Symbol')

stock_data_raw.columns = stock_data_raw.columns.droplevel()

# collect correct header names (actual stocks)

column_names = list(stock_data_raw)

stock_data_raw.tail()

# hack to remove mult-index stuff

stock_data_raw = stock_data_tmp[['Symbol', 'Date', 'Close']]

stock_data_raw = stock_data_raw.pivot('Date','Symbol')

stock_data_raw.columns = stock_data_raw.columns.droplevel(-1)

stock_data_raw.columns = column_names

# replace NaNs with previous value

stock_data_raw.fillna(method='bfill', inplace=True)

stock_data_raw.tail()

Make a copy of the data set before transforming it

stock_data = stock_data_raw.copy()

Plot paired stocks on different axes

plt.figure(figsize=(12,5))

ax1 = stock_data['FDX'].plot(color='green', grid=True, label='FDX')

ax2 = stock_data['UPS'].plot(color='purple', grid=True, secondary_y=True, label='UPS')

h1, l1 = ax1.get_legend_handles_labels()

h2, l2 = ax2.get_legend_handles_labels()

plt.legend(h1+h2, l1+l2, loc=2)

plt.show()

plt.figure(figsize=(12,5))

ax1 = stock_data['KO'].plot(color='green', grid=True, label='KO')

ax2 = stock_data['PEP'].plot(color='purple', grid=True, secondary_y=True, label='PEP')

h1, l1 = ax1.get_legend_handles_labels()

h2, l2 = ax2.get_legend_handles_labels()

plt.legend(h1+h2, l1+l2, loc=2)

plt.show()

Normalize data

In order to compare moves between differently priced assets, we need to normalize the data.

According to Wikipedia,

In statistics and applications of statistics, normalization can have a range of meanings. In the simplest cases, normalization of ratings means adjusting values measured on different scales to a notionally common scale, often prior to averaging.

https://en.wikipedia.org/wiki/Normalization_(statistics)

Percent Change And Cumsum

A very simple way to do this is to transform price data into percentage changes and apply a rolling sum, known as a cumulative sum.

def normalize_and_accumulate_series(data):

# take tail to drop head NA

return data.pct_change().cumsum()

stock_data['FDX'] = normalize_and_accumulate_series(stock_data['FDX'])

stock_data['UPS'] = normalize_and_accumulate_series(stock_data['UPS'])

stock_data['KO'] = normalize_and_accumulate_series(stock_data['KO'])

stock_data['PEP'] = normalize_and_accumulate_series(stock_data['PEP'])

# remove first row with NAs

stock_data = stock_data.tail(len(stock_data)-1)

stock_data.head()

Plot paired stocks on same axes

fig, ax = plt.subplots(figsize=(12,5))

plt.plot(stock_data['FDX'], color='green', label='FDX')

plt.plot(stock_data['UPS'], color='purple', label='UPS')

ax.grid(True)

plt.legend(loc=2)

plt.show()

fig, ax = plt.subplots(figsize=(12,5))

plt.plot(stock_data['KO'], color='purple', label='KO')

plt.plot(stock_data['PEP'], color='green', label='PEP')

ax.grid(True)

plt.legend(loc=2)

plt.show()

Getting some statistical measurements

# pip install scipy

# pip install statsmodels

from statsmodels.tsa.stattools import coint

def corr(data1, data2):

"data1 & data2 should be numpy arrays."

mean1 = data1.mean()

mean2 = data2.mean()

std1 = data1.std()

std2 = data2.std()

corr = ((data1*data2).mean()-mean1*mean2)/(std1*std2)

return corr

stock_name_1 = 'KO'

stock_name_2 = 'PEP'

score, pvalue, _ = coint(stock_data[stock_name_1], stock_data[stock_name_2])

correlation = corr(stock_data[stock_name_1], stock_data[stock_name_2])

print('Correlation between %s and %s is %f' % (stock_name_1, stock_name_2, correlation))

print('Cointegration between %s and %s is %f' % (stock_name_1, stock_name_2, pvalue))

stock_name_1 = 'UPS'

stock_name_2 = 'FDX'

score, pvalue, _ = coint(stock_data[stock_name_1], stock_data[stock_name_2])

correlation = corr(stock_data[stock_name_1], stock_data[stock_name_2])

print('Correlation between %s and %s is %f' % (stock_name_1, stock_name_2, correlation))

print('Cointegration between %s and %s is %f' % (stock_name_1, stock_name_2, pvalue))

Measuring separatation and spikes highlights

This is straighforward, we simply subtract the two related and normalized series

fig, ax = plt.subplots(figsize=(12,5))

plt.plot(stock_data['FDX'] - stock_data['UPS'], color='purple', label='Diff FDX minus UPS')

ax.grid(True)

ax.axhline(y=0, color='black', linestyle='-')

plt.legend(loc=2)

plt.show()

fig, ax = plt.subplots(figsize=(12,5))

plt.plot(stock_data['KO'] - stock_data['PEP'], color='purple', label='Diff KO minus PEP')

ax.grid(True)

ax.axhline(y=0, color='black', linestyle='-')

plt.legend(loc=2)

plt.show()

Designing spike thresholds

# get the original data set

stock_data = stock_data_raw.copy()

def normalize_series(data):

# take tail to drop head NA

return data.pct_change()

stock_data['FDX'] = normalize_series(stock_data['FDX'])

stock_data['UPS'] = normalize_series(stock_data['UPS'])

stock_data['KO'] = normalize_series(stock_data['KO'])

stock_data['PEP'] = normalize_series(stock_data['PEP'])

# remove first row with NAs

stock_data = stock_data.tail(len(stock_data)-1)

stock_data.head()

fig, ax = plt.subplots(figsize=(12,5))

plt.plot(stock_data['FDX'] - stock_data['UPS'], color='purple', label='Diff FDX minus UPS')

ax.grid(True)

ax.axhline(y=0, color='black', linestyle='-')

ax.axhline(y=0.02, color='red', linestyle='-')

ax.axhline(y=-0.02, color='red', linestyle='-')

plt.legend(loc=2)

plt.show()

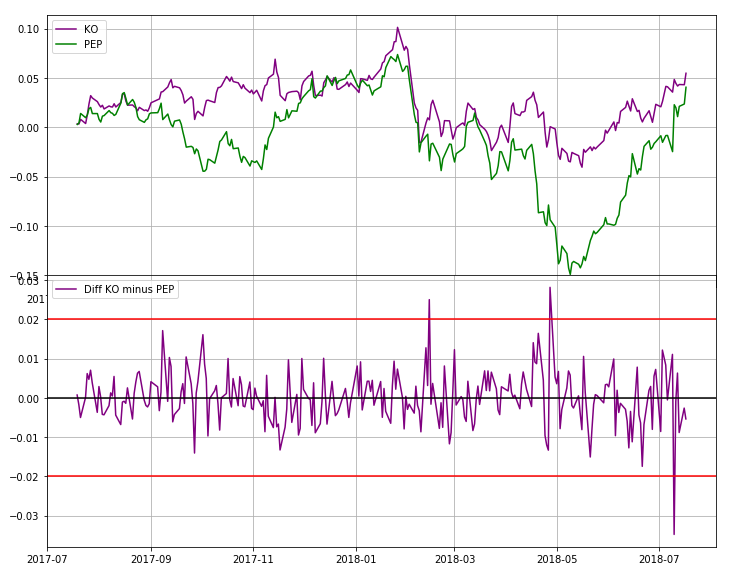

fig, ax = plt.subplots(figsize=(12,5))

plt.plot(stock_data['KO'] - stock_data['PEP'], color='purple', label='Diff KO minus PEP')

ax.grid(True)

ax.axhline(y=0, color='black', linestyle='-')

ax.axhline(y=0.02, color='red', linestyle='-')

ax.axhline(y=-0.02, color='red', linestyle='-')

plt.legend(loc=2)

plt.show()

Manuel Amunategui - Follow me on Twitter: @amunategui